The Chart du Jour

USD/JPY: A Longer Term Perspective

Apparently an eleven year long slump in the Japanese economy does not a bargain make. Somehow, the Japanese have mastered how to create a poor economy with strong debt-deflationary pressures while maintaining high retail prices at the same time. Despite their domestic problems, they have similarly mastered maintaining a large trade surplus with the U.S. that creates a continuous flow of dollars earned abroad that need to be hedged back into yen. This dollar overhang then becomes the primary reason that the yen has such a hard time depreciating as one might otherwise expect it should.

Someday, somehow this situation has to change. With the recent jump from 101 to 109 in USD/JPY we think such a change has probably already begun. To date the Japanese have tried every possible methodology of artificial stimulus to get their economy moving again EXCEPT for an outright devaluation of their currency. By recently adopting the decision to bypass the capital markets for part of their government funding needs, the Japanese have sent the markets a powerful message: they are now willing to resort to outright monetization of their debt, even though they would never explicitly express it in such terms.

In the chart below, we have drawn the Fibonacci retracement lines between the 1995 low and the 1998 high in USD/YEN. To our eye, these lines do not 'fit' the intervening price action of the market particularly well. To us this means that the 1998 high was not a significant and lasting one.

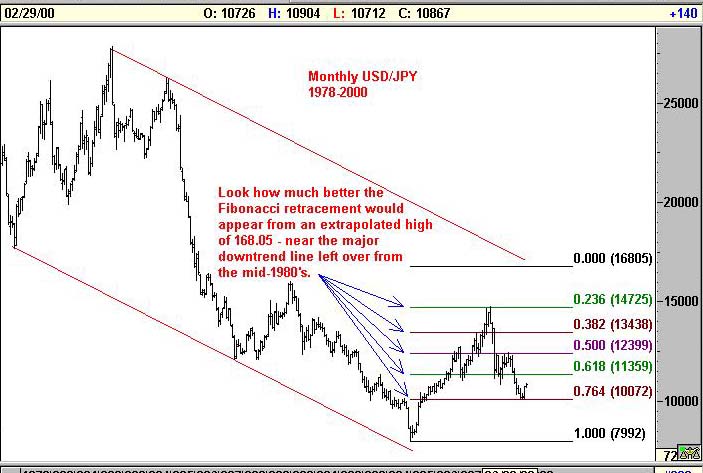

Now, in lieu of using the 1998 USD/JPY high at 147.95, we have measured in the chart below our Fibonacci retracements from an extrapolated high at 168.05. Note how much better the Fibonacci retracements would 'fit' USD/JPY's price action throughout the 1995-2000 period if such a high were eventually to transpire. To us this means that longer term 168.05 is indeed a level that we are headed to.

Is this hugely bullish the U.S. markets as a whole? To the extent that the U.S. dollar continues to be the global investment of choice, it cannot help but be initially supportive of our fixed income and equity markets. But it also holds the seeds of its own destruction. The higher the dollar goes, and the more capital that migrates to our shores, the more wealth will be created here, the more our trade deficit will balloon, and the more domestic wealth-induced inflationary pressures the Fed will be facing.

In 1928 the Fed cut rates in order to try to dissuade capital from coming to our shores and help support the British pound. The Fed created instead a domestic equity buying spree, and more capital came to our shores equity-bound, not less.

In 1998 the Fed cut rates for a different reason: to prevent the global debt and derivatives markets from completely seizing up. Once again, an equity buying binge was an unforseen result.

Now in 2000 we risk something a bit the reverse. For domestic reasons, the Fed must now raise interest rates, but the more they do so, the more they will undermine the relative attractiveness of equities vis a vis fixed income. The more they are also likely drive up the value of the U.S. dollar and undermine the relative competitive position of U.S. industry in the export market. Eventually we risk seeing an entropic "black hole" for U.S. equities as corporate profitability -- faced with both higher interest rates and a higher dollar -- wanes. Perhaps that is why the export-heavy Dow Jones Industrial Index is already lagging so badly.

As much as we would love to wave the flag and herald a "new paradigm" in American business, the more scared we become of the global imbalances that currently exist and which seem to be careening out-of-control. We can bring ourselves to be bullish the U.S. dollar, but we cannot bring ourselves to be secularly bullish a U.S. equity market that someday soon is going to get truly squeezed.

Am I wrong about this? Please post your comments in the Sandspring.com chatroom.

Thank you for visiting Sand Spring Advisors LLC, Inc. We hope to hear from you again soon. For more information on Sand Spring Advisors actual programs, services, or to request a copy of a Disclosure Document, please phone us at 973 829 1962, FAX your request to 973 829 1962, or e-mail us at

info@Sandspring.com| Corporate Office: 10 Jenks Road, Morristown, NJ 07960 Phone: 973 829 1962 Facsimile: 973 829 1962 |

Best Experienced with

The material located on this website is also the copyrighted work of Sand Spring Advisors LLC. No party may copy, distribute or prepare derivative works based on this material in any manner without the expressed permission of Sand Spring Advisors LLC

This page and all contents are Copyright © 1999 by Sand Spring Advisors, LLC, Morristown, NJ