The Chart du Jour

The Nasdaq market was feigning a possible C wave rally late last week within what is clearly a complex 4th wave period of retrenchment that started back on April 4th., 2000.

Could this actually transpire? Sure it could. 4th waves by definition are complex affairs that can take considerable time to finish and are filled with constant false moves and opportunities to elect too tightly placed stop-losses.

But do we think this is the highest probability path? No. All of our pattern match analysis of financial sector stocks and the Dow Jones Industrials suggests something more sinister is brewing. As such, we see the recent Nasdaq effort to rally being more of a "hang mode" flat 4th. wave than a more typical A-B-C formation. Anecdotally, even Microsoft couldn't get a solid head of steam up behind it after good news on its court battle.

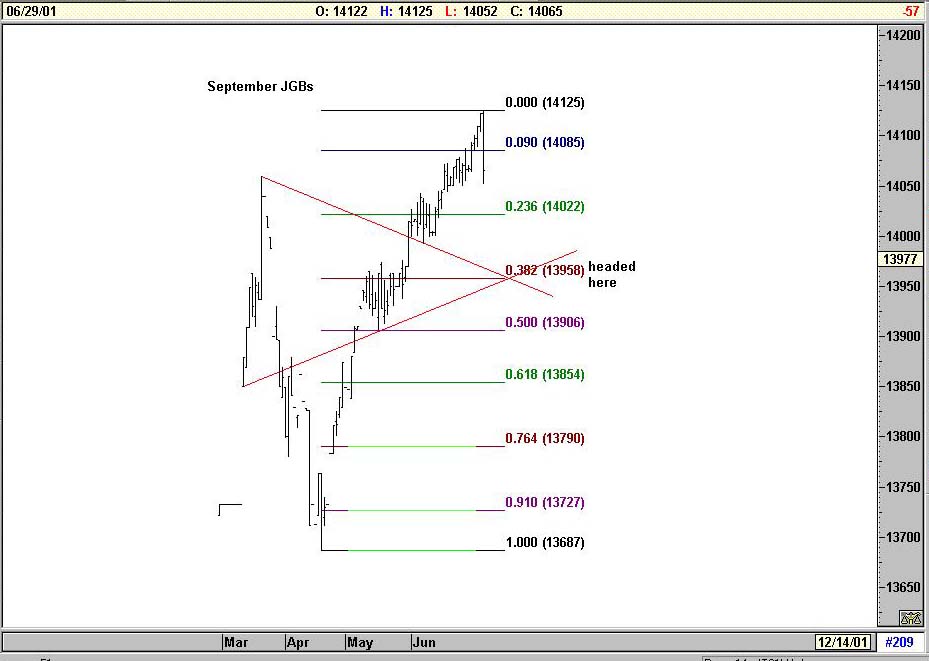

On top of these perspectives, let's add to the mix of our analysis the fact that Japanese Government Bond futures made an "outside-day key reversal" Friday.

Now maybe this happened because equity markets were rallying in Japan and elsewhere on renewed prospects of global growth, but an outside-day key reversal (defined as new highs for a move followed by a close below the prior day's low) is an outside-day key reversal, and it is an important technical formation to take note of.

I have long argued that the world economic situation cannot be fundamentally "in balance" as long as Japanese short term interest rates are at the near-zero levels that they have been for some time now, and 10-year government securities there yield less than 1.8%. Japan still controls 25% of the world's global wealth, and much of that wealth is tied up in the JGB market for a variety of cultural and historic reasons. My question is this: How can any market around the world be deemed truly safe if all this money stands at risk of getting wiped out?

Just read this short article from RiskCenter.com that appeared back on May 31st and tell me that we can somehow afford not to pay close attention to the price behavior of JGBs:

Japan's banks have more than doubled their holdings of central government bonds in the past two years, leaving them with a record high level of exposure to the bond market--The dramatic rise has triggered concern within the Japanese government about the vulnerability of the banks' capital bases to any bond market swing.We do not fully pretend to know all the details behind Friday's sharp and dramatic JGB reversal. But we do think it is important to take note of. If global equity markets were to launch anything of a substantive rally, then the flip side of such a move could easily be that the JGB market stands at substantive risk of being destroyed. And if all that wealth in JGBs evaporates, will the world really be that better off then than it is now? We think not. Despite a great deal of complacency out there, we still see global financial markets as extraordinarily dangerous at this time.Bank of Japan data shows that at the end of March, the banks held Y73,000bn ($608bn) of Japanese government bonds (JGB), up from Y46,000bn the previous year, and Y32,000bn in March 1999.

This means that JGBs now represent about a tenth of the banks' total assets -- double the level two years ago, and considerably higher than their equity portfolio.

If interest rates suddenly started rising, this could leave the banks nursing large portfolio losses.

Brian Waterhouse, banks analyst at HSBC Securities, said: "If the government comes out with decisive measures to deal with bad loans -- which everybody says is holding the economy back -- then interest rates would rise, suggesting the banks could face quite heavy value losses."

However, he pointed out that the banks had little choice but to increase bond holdings due to almost non-existent demand for loans and a rise in deposits, despite near-zero interest rates on deposit accounts.

"Banks have had no problems raising funds, but have had difficulty finding profitable places to invest these funds. Government bonds are zero risk in BIS terms and at least have a yield," he said.

The sharp rise in bond holdings has put the banks in a tricky position as far as the accuracy of their earnings forecasts for this financial year, announced last week, are concerned.

Most of the banks have based their earnings projections on average economic growth of 2 percent, indicating that if their expectations came true, interest rates would rise, bond yields would fall and their earnings forecasts could suffer.

Hakuo Yanagisawa, the Financial Reform Minister, said in parliament last week that "the rise in banks' JGB holdings is remarkable".

He said that although the situation was not "an emergency", he did have concerns "because the market risk related to holding bonds is increasing".

However, the trend has also brought some relief for the central government. The heavy purchases of JGBs by the banks are a key factor holding down long- and short-term interest rates.

How Your Articles Are Delivered

Upon the processing of your credit card or the receipt of a personal check, Sand Spring will e-mail you the articles requested as a Word attachment, and also provide you with a WWW address and password to view the article on the web without using Word should you so desire. Confirmation of your order will be immediate, and the actual article will follow by e-mail typically within a few hours and in all cases before the opening of NYSE trading on the following day.

Ordering by Credit Card:

Our shopping cart is designed for both physical and subscription products, so do not be confused too much when it asks you for a shipping address. A correct address is important only for credit card authorization purposes. Your e-mail information is the most important piece of information to us for proper delivery of your article(s).

Sand Spring Advisors provides information and analysis from sources and using methods it believes reliable, but cannot accept responsibility for any trading losses that may be incurred as a result of our analysis. Individuals should consult with their broker and personal financial advisors before engaging in any trading activities, and should always trade at a position size level well within their financial condition. Principals of Sand Spring Advisors may carry positions in securities or futures discussed, but as a matter of policy will always so disclose this if it is the case, and will specifically not trade in any described security or futures for a period 5 business days prior to or subsequent to a commentary being released on a given security or futures.

If you order by credit card, your credit card will be billed as "Sand Spring Advisors LLC"

Take me back to the Sand Spring Home Page

Comments or Problems

Thank you for visiting Sand Spring Advisors LLC, Inc. We hope to hear from you again soon. For more information on Sand Spring Advisors actual programs, services, or to request a copy of a Disclosure Document, please phone us at 973 829 1962, FAX your request to 973 829 1962, or e-mail us at information@Sandspring.com

| Corporate Office: 10 Jenks Road, Morristown, NJ 07960 Phone: 973 829 1962 Facsimile: 973 829 1962 |

Best Experienced with

The material located on this website is also the copyrighted work of Sand Spring Advisors LLC. No party may copy, distribute or prepare derivative works based on this material in any manner without the expressed permission of Sand Spring Advisors LLC

This page and all contents are Copyright © 2000 by Sand Spring Advisors, LLC, Morristown, NJ